United States Bakeware Market Size, Share, Forecast & Trends Analysis Report (2025-2033)

Market Overview

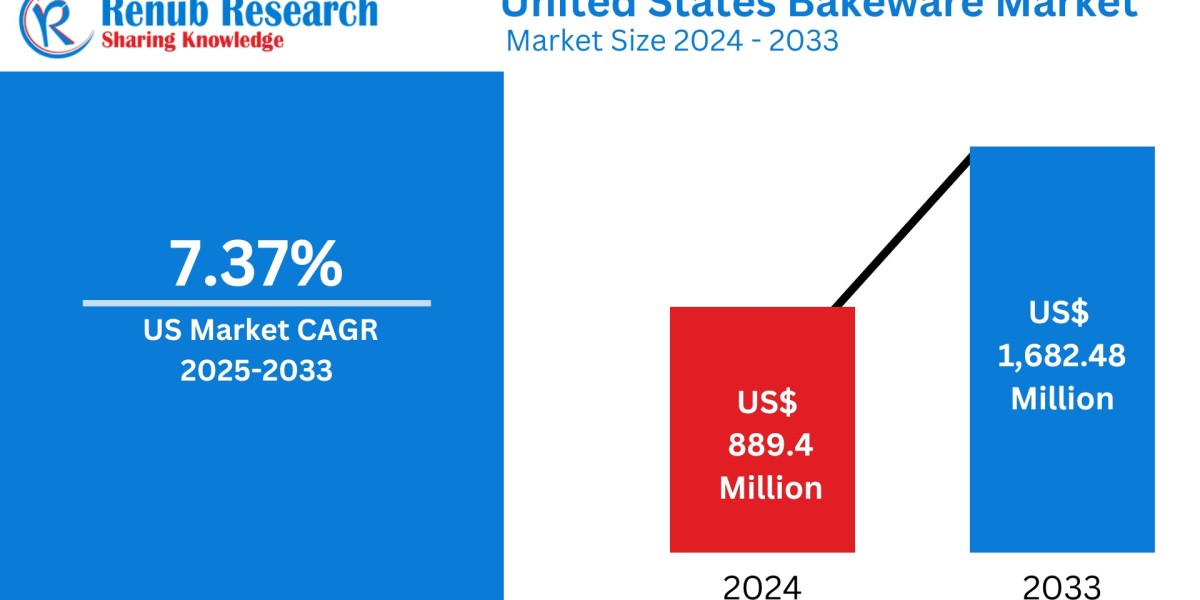

The United States Bakeware Market reached a valuation of US$ 889.4 million in 2024 and is forecasted to grow at a CAGR of 7.37% during the period 2025 to 2033, ultimately reaching US$ 1,682.48 million by 2033. The surge in home baking, evolving consumer preferences for non-stick and sustainable bakeware, and the massive influence of cooking shows and social media platforms have significantly accelerated the market growth. Consumers are increasingly seeking durable, stylish, eco-friendly, and easy-to-maintain bakeware products, leading to high demand for materials like silicone, ceramic, and stainless steel.

Market Definition and Dynamics

Bakeware encompasses utensils and equipment used in baking, such as pans, trays, molds, and dishes. These items are fabricated using a wide range of materials—aluminum, stainless steel, stoneware, glass, and more—each offering specific benefits in terms of durability, heat retention, and food safety.

The current market dynamics reflect a shifting consumer mindset—from mere functionality to enhanced aesthetics, sustainability, and innovation. This transformation is particularly evident in the increasing preference for non-toxic, BPA-free, dishwasher-safe, and multi-functional bakeware items, especially in households and growing artisanal businesses.

Key Market Drivers

1. Surging Trend of Home Baking

Home baking in the U.S. has transitioned from a hobby to a lifestyle, fueled by pandemic habits and sustained by online influencers, recipe content creators, and baking competitions. A Packaged Facts 2022 survey noted that 31% of U.S. consumers bake at least once a week, while 24% bake at least once or twice a month, demonstrating a stable consumer base.

This trend has prompted increased demand for innovative and sustainable bakeware including non-stick pans, decorative molds, and eco-friendly baking trays.

2. E-commerce Boom and Direct-to-Consumer Accessibility

The growing penetration of online retail channels has democratized access to a wide range of bakeware products. Leading platforms and specialty stores are offering exclusive collections, bundle deals, and influencer collaborations, boosting online conversions.

Brands like Pillsbury, Our Place, and Betty Crocker have leveraged digital platforms to launch exclusive and themed bakeware kits, appealing to consumers looking for convenience and creativity in their culinary pursuits.

3. Product Innovation and Material Advancements

Bakeware manufacturers are increasingly launching products that offer superior heat resistance, durability, and safety. Materials such as silicone, ceramic-coated metal, carbon steel, and glass are gaining traction due to their non-toxic and performance-enhancing attributes.

In July 2024, KitchenAid launched a licensed metal bakeware series, reflecting consumer demand for visually appealing and functionally superior products.

Related Report

United States Bottled Water Market

United States School Furniture Market

Key Market Challenges

1. Intense Competition from Low-Cost Imports

Increased imports from cost-competitive countries such as China have created price pressure on U.S.-based manufacturers. These products, while more affordable, may compromise quality, impacting brand loyalty and long-term market stability.

2. Volatility in Raw Material Prices

Fluctuating prices of core materials like aluminum and stainless steel, driven by supply chain issues, global conflicts, or inflation, impact production costs. This variability poses a challenge in maintaining consistent pricing and profit margins.

Segmental Insights

By Product Type

- Tins & Trays: Most commonly used for cookies and cakes. High demand for non-stick and eco-friendly options is shaping this segment.

- Cups: Silicone and biodegradable paper cups are driving innovation in the cupcake and muffin segment.

- Molds and Pans: Creative designs for themed baking and portion-controlled servings are increasingly in demand.

- Rolling Pins & Others: Traditional tools remain popular, particularly among hobbyist bakers.

By Material

- Stainless Steel: Preferred for its rust resistance, durability, and chemical-free baking surface.

- Aluminum: Valued for its light weight and heat conductivity; coated aluminum is gaining traction to overcome concerns about food interaction.

- Ceramic and Stoneware: Eco-conscious and aesthetically appealing, ceramic bakeware aligns with modern kitchen design trends.

- Glass: Offers transparency and reusability, appealing to health-conscious consumers.

By End User

- Commercial Segment: With the rise of boutique bakeries, cafes, and patisseries, demand for high-performance, large-capacity bakeware has increased.

- Household Segment: Home users are increasingly opting for multi-functional, non-stick, and branded bakeware, often influenced by lifestyle trends and social media.

Regional Insights

East United States

Urban centers like New York and Boston are hubs for gourmet baking. Specialty baking stores and premium bakeware are in high demand. Brands like Nordic Ware have capitalized on this trend with innovative product launches.

West United States

Environmental consciousness is shaping consumer choices. High preference for non-toxic, sustainable bakeware (e.g., silicone and ceramic) in states like California and Washington.

North United States

Stronghold of the commercial baking sector with a dense population of bakeries and cafes. Demand for durable, high-capacity bakeware for professional use is dominant.

South United States (Note: Expand this section in your final draft)

Growing suburban populations and cultural diversity are encouraging culinary experimentation, contributing to the rising popularity of both traditional and modern bakeware tools.

Distribution Channel Insights

- Online: Rapid growth due to convenience, variety, and personalized marketing. Brands like Our Place and Farberware are leveraging DTC models to build loyal customer bases.

- Offline: Departmental and specialty stores continue to drive sales through touch-and-feel experiences and in-store promotions.

Competitive Landscape

Leading players are focusing on collaborations, themed launches, and product innovations to stay competitive. Key players include:

- Groupe SEB

- Wilton Brands LLC

- Newell Brands Inc.

- Meyer Corporation U.S.

- Emile Henry USA

- Werhahn Group (ZWILLING- Staub)

- USA Pan

- Le Creuset

- Nordic Ware

- Caraway

Each company is evaluated across four dimensions:

- Company Overview

- Key Executives

- Recent Developments

- Revenue Analysis

United States Bakeware Market – Key Highlights

Feature | Details |

Base Year | 2024 |

Forecast Period | 2025–2033 |

Market Size (2024) | US$ 889.4 Million |

Market Size (2033) | US$ 1,682.48 Million |

CAGR (2025–2033) | 7.37% |

Segment Covered | Product, Material, End User, Distribution Channel, Region |

Coverage | East, West, North, South U.S. |

Format | PDF & Excel (Editable PPT/Word on request) |

Support | 1-Year Post-Sale Analyst Support |

Customization Scope

Renub Research offers 20% free customization with flexibility for:

- Additional countries or regions

- Deeper segmentation

- Company profiling (up to 10 more firms)

- Market entry strategies

- Trade and production analysis

Purchase Options

License Type | Price |

Dashboard (Excel) | $2,490 |

Single User (PDF) | $2,990 |

Five Users (PDF + Excel) | $3,490 |

Corporate License (Multi User) | $3,990 |

Contact Us

? USA: +1-678-302-0700

? India: +91-120-421-9822

? Email: info@renub.com

? Website: www.renub.com